In 2025, Brenntag SE once again operated in a global market environment that remained challenging. Geopolitical tensions, an increasingly fragmented trading landscape and U.S. trade policy actions led to elevated uncertainty in international trade and curbed investment. Higher U.S. tariffs, a stronger euro and increasing trade conflicts clouded the economic outlook, particularly in Europe and Asia. Progressively normalizing inflation had a positive impact, as did the gradual easing of central banks’ monetary policy, although interest rates remained restrictive overall. This supported consumer spending to some extent. Nevertheless, global economic growth remained subdued overall.

Economic performance varied from region to region again. In the U.S., the economy proved to be relatively robust despite protectionist measures, but lost momentum during the course of the year in the face of high financing terms and political uncertainty. The European Economic Area continued to be marked by structural challenges, weak external demand and trade tensions, which impacted negatively on international competitiveness. Several Asian economies posted a stable performance and remained the most important global growth drivers in 2025, while China continued to suffer as a result of systemic challenges and weak domestic demand. Latin America painted a mixed picture, with growth subdued overall. On the whole, global economic performance was once again shaped by a mix of growth drivers and headwinds. According to estimates by the International Monetary Fund, the global economy grew by around 3.2% in real terms in 2025, a slightly weaker rate of growth than in the previous year (3.3%).1)

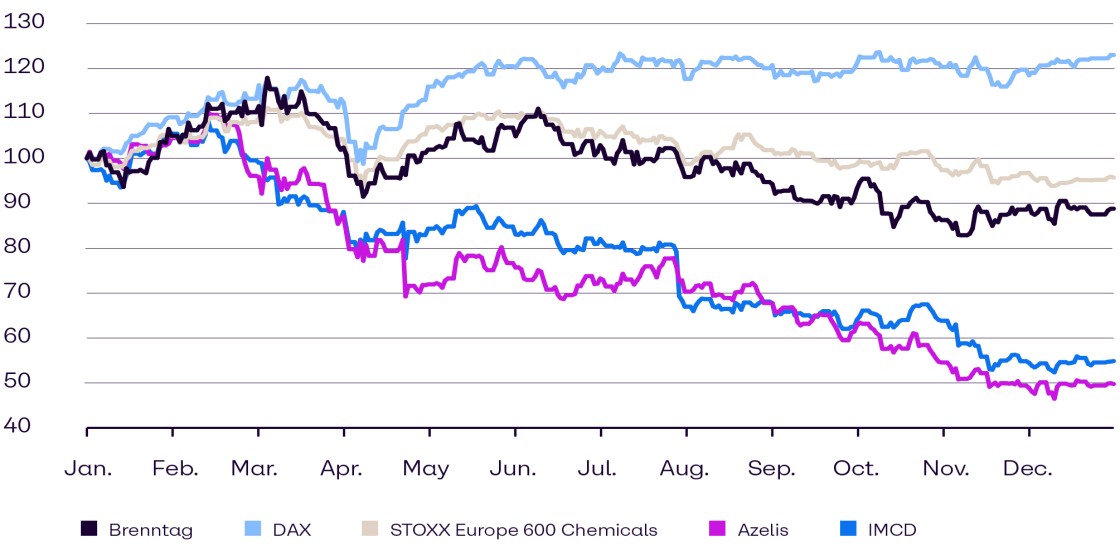

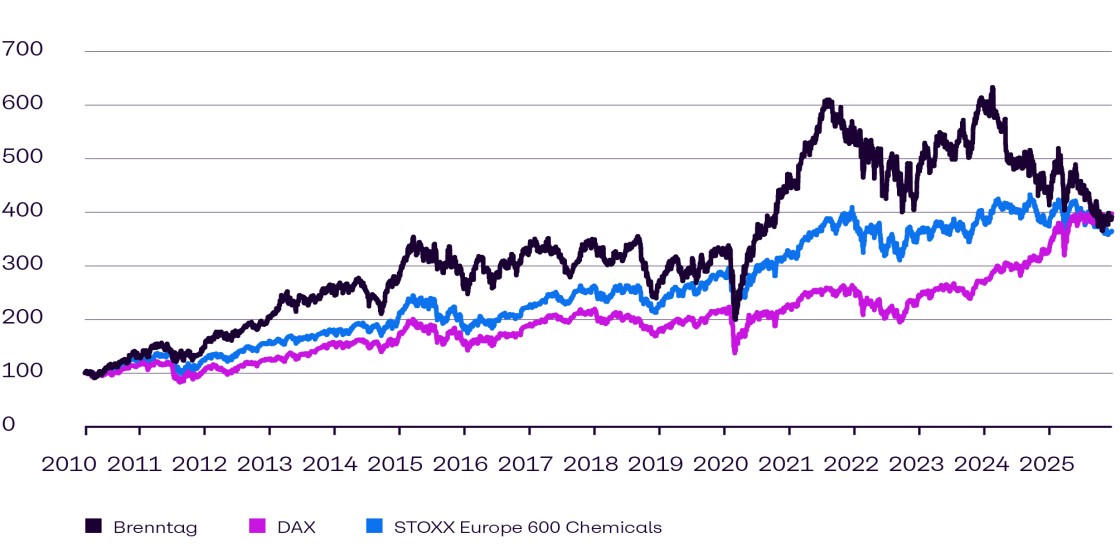

In the same period, global equity markets continued their positive performance. The major central banks gradually loosened their previously restrictive monetary policy in 2025. Both the ECB and the Fed cut key interest rates several times due to falling inflation rates and declining inflation expectations. The ECB reduced the deposit rate to 2.0% and kept it on hold from the middle of the year onwards, while inflation in the euro zone rose slightly from 2.1% to 2.2%. The Fed lowered the target range for the federal funds rate from 4.5% to 4.0% but maintained a restrictive stance overall despite the adjustments. Global equity markets also received a significant boost from the strong earnings performance from U.S. technology firms in the reporting period. Thus, Germany’s leading index reached a new all-time high of 24,650 points in July 2025 and ended financial year 2025 up by 23%.

1) Source: IMF (International Monetary Fund) World Economic Outlook Update January 2026.